Back to Basics #5

Stablecoins have quietly become one of the most important innovations in cryptocurrency, yet many people still think of them as just "dollar tokens on chain." The reality is far more significant. Stablecoins are emerging as critical financial infrastructure, powering everything from cross-border payments to business treasury operations to decentralized finance applications.

This Back to Basics guide explains what stablecoins are, why they exist, how businesses actually use them today, and where this technology is heading.

What Are Stablecoins?

A stablecoin is a cryptocurrency designed to maintain a stable value, typically pegged to a fiat currency like the U.S. dollar. While Bitcoin and other cryptocurrencies can fluctuate dramatically in price, stablecoins aim to stay at roughly $1.00 per token, making them suitable for payments, savings, and business operations where price stability matters.

Think of stablecoins as digital dollars that move at the speed of the internet. You get the benefits of cryptocurrency (instant transfers, global accessibility, transparent transactions) without the volatility that makes Bitcoin unsuitable for paying your rent or settling an invoice.

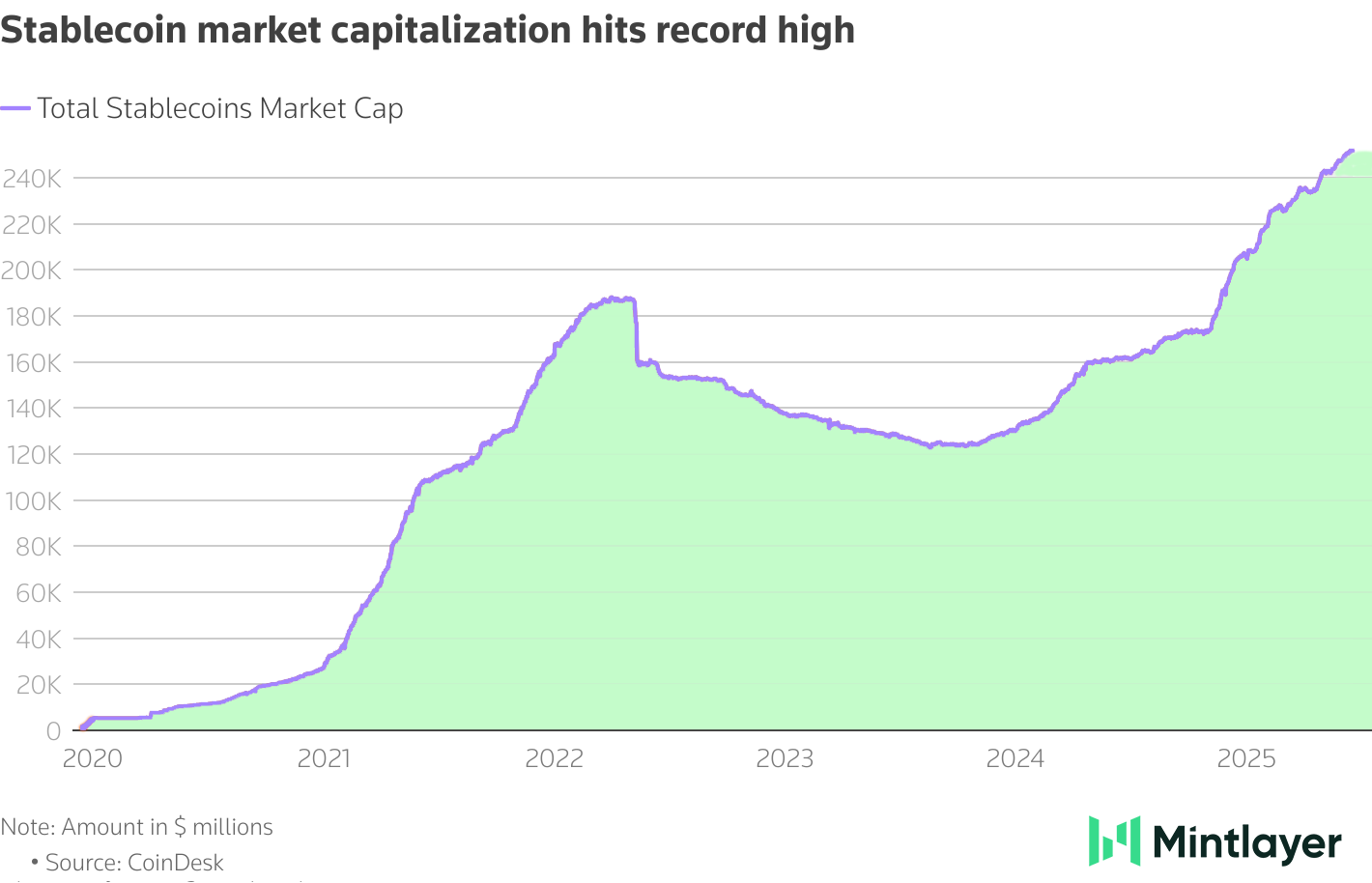

The stablecoin market has grown to over $250 billion in total value, with trillions of dollars in annual transaction volume. This isn't speculative trading. These are real payments, business operations, and financial flows happening on-chain.

Why Stablecoins Exist

Traditional payment systems weren't designed for the digital, global, 24/7 economy we live in today. Several fundamental problems make legacy banking inefficient for modern needs.

Speed and availability. Banks operate during business hours and take days to settle cross-border transactions. A wire transfer can take one to three business days to complete. Stablecoins settle in seconds, any time of day, including weekends and holidays.

Cost. International wire transfers often cost $25 to $50 per transaction, with additional correspondent bank fees. In many Asian corridors, banks take several percentage points off each transfer. Stablecoin transactions typically cost pennies, regardless of amount.

Accessibility. Roughly 1.4 billion adults worldwide lack access to traditional banking. Opening a bank account requires documentation, credit history, and physical proximity to branches. Anyone with an internet connection can create a stablecoin wallet and start transacting immediately, with no permission required.

Transparency. Wire transfers provide limited visibility into where your money is and when it arrives. With stablecoins, every transaction is recorded on a public blockchain. You can track exactly where your payment is and when it settles.

Programmability. Traditional money can't execute logic automatically. Stablecoins integrate into smart contracts, enabling automated payments triggered by specific conditions, scheduled transfers, and complex business logic that would require manual intervention with banks.

Types of Stablecoins & How They Are Pegged

Stablecoins are designed to "peg" their value to a specific asset or basket of assets, most commonly fiat currencies like the U.S. dollar. This pegging mechanism is what allows stablecoins to combine the advantages of cryptocurrency (speed, transparency, programmability, global accessibility) with the price stability of traditional currencies. The goal is simple: maintain a stable exchange rate so that one stablecoin equals one dollar, regardless of broader crypto market volatility.

However, achieving and maintaining this peg requires different approaches, each with distinct trade-offs in terms of decentralization, capital efficiency, and reliability. The method used to maintain the peg fundamentally shapes how the stablecoin operates, how much trust users need to place in the issuer, and how resilient the token is during market stress. Understanding these different pegging mechanisms helps explain why some stablecoins have achieved widespread adoption and institutional trust, while others have collapsed spectacularly.

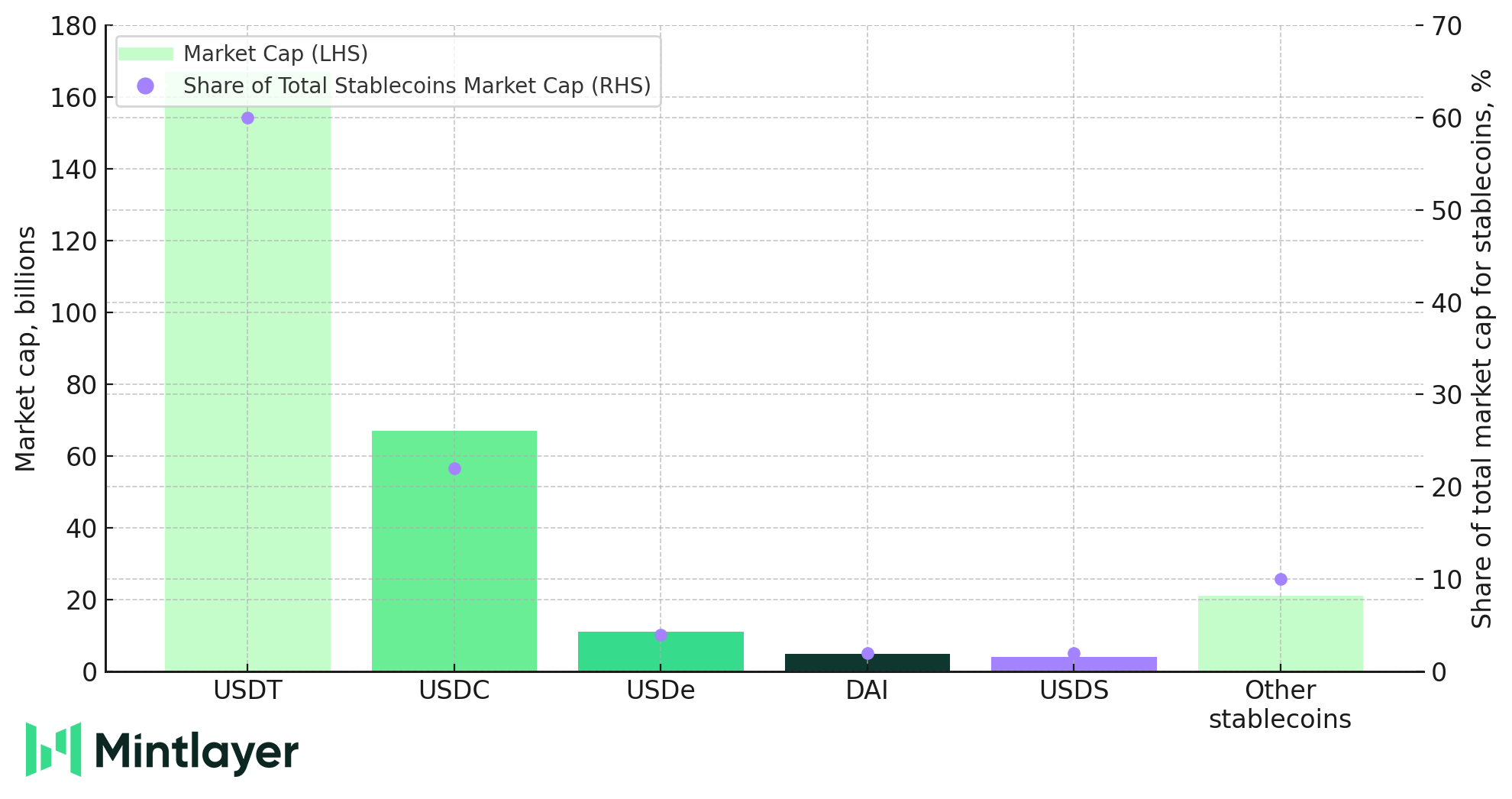

Fiat-backed stablecoins are the most common and trusted. For every stablecoin issued, the company holds equivalent fiat currency in reserve. USDC and USDT fall into this category. They maintain their peg through direct backing, regular audits, and the ability to redeem tokens for dollars. They're the most straightforward model and what businesses typically prefer.

Crypto-backed stablecoins use cryptocurrency as collateral. DAI is the most well-known example. These are over-collateralized to absorb price volatility in the collateral. They're more decentralized than fiat-backed options but more complex and dependent on the health of underlying crypto assets.

Algorithmic stablecoins attempt to maintain their peg through supply and demand mechanisms without holding reserves. This model has largely fallen out of favor after several high-profile failures, including TerraUSD's collapse in 2022.

The clear winner in terms of adoption and trust has been fiat-backed stablecoins, which combine cryptocurrency's speed and accessibility with traditional finance's stability and regulatory clarity.

How Stablecoins Are Actually Used Today

Beyond trading on crypto exchanges, stablecoins power real economic activity across multiple sectors.

Cross-border payments and remittances. Workers sending money home used to lose 5% to 10% of each transfer to fees and exchange rate markups. Stablecoins reduce that cost to near zero while delivering funds instantly. In regions where traditional banking is expensive or unreliable, adoption has been rapid and practical.

Business-to-business payments. Companies operating across multiple countries face expensive wire fees, multi-day settlement times, and complex reconciliation. Stablecoins enable businesses to pay suppliers and partners globally with instant settlement, lower costs, and complete transaction visibility.

Global payroll. Companies with distributed teams can process bulk payroll in minutes instead of days. Employees can receive payment in stablecoins and either hold them, convert to local currency, or spend directly.

Treasury and liquidity management. Businesses are holding portions of working capital in stablecoins for faster internal transfers between subsidiaries, light foreign exchange hedging, and access to yield opportunities. Stablecoins move between company entities globally in real time with automated controls and transparent audit trails.

Trade finance and supply chain. Tokenizing invoices and purchase orders enables automatic payment release upon delivery or milestone completion. Suppliers get faster cash flow while buyers gain visibility and automated dispute resolution.

DeFi protocols. Stablecoins serve as the base currency for decentralized finance applications, enabling lending, borrowing, and yield generation without requiring users to hold volatile assets.

The Bottlenecks Preventing Broader Adoption

Despite proven utility, stablecoins haven't yet reached mainstream business adoption. The technology works. The hesitation comes from practical and regulatory concerns.

Regulatory uncertainty tops the list. Most businesses want clear regulatory treatment before moving significant volume, especially when operating across multiple jurisdictions with different rules. The regulatory landscape remains fragmented.

Accounting and audit frameworks need standardization. CFOs ask reasonable questions about classification, internal controls, and how auditors will view stablecoin holdings. Until these frameworks are clearly established, many businesses move cautiously.

Infrastructure integration remains incomplete. Not every payment service provider or merchant system is ready to settle in stablecoins today. Finance and operations teams want clean settlement flows, clear reporting, and simple reconciliation. If handling stablecoins requires managing ten manual steps, companies stick with systems they know.

These aren't technical problems. They're integration, education, and regulatory challenges that will resolve as the market matures.

Enterprise Stablecoin Infrastructure

Recognizing these bottlenecks, specialized infrastructure is emerging to make stablecoin adoption practical for businesses without requiring them to rebuild financial operations.

Mintlayer Web Services (MWS) addresses this gap, providing compliant stablecoin infrastructure designed for enterprise use. Rather than forcing companies to navigate blockchain complexity, MWS offers solutions for common business needs.

Global payroll and contractor payouts become straightforward. Upload a CSV or use the API to pay distributed teams in minutes. The system handles per-jurisdiction tax documentation, automated pay stubs, and optional off-ramps for local currency conversion. Audit trails, approval workflows, and role-based controls keep HR and finance aligned.

Cross-border B2B payments replace slow wire transfers with stablecoin settlement. Set payment terms, attach invoices, and trigger release automatically. Companies gain lower fees, 24/7 availability, and automated reconciliation back into existing accounting systems.

Trade finance and supply chain settlement benefit from tokenized invoices and purchase orders. Payment releases automatically on delivery, giving suppliers faster cash flow while buyers gain visibility and streamlined dispute resolution.

Corporate treasury and liquidity management allow companies to hold working capital in stablecoins for faster internal transfers. Move funds between subsidiaries in real time, set spending limits, and connect to approved yield venues with appropriate guardrails.

These applications show how stablecoins move from theoretical benefits to practical business tools when infrastructure handles complexity on behalf of users.

What This Means for the Future of Money

Stablecoins represent the clearest path from cryptocurrency experimentation to real financial infrastructure. They combine the stability businesses need with the efficiency blockchain enables.

As more businesses discover that stablecoins solve real problems better than existing alternatives, adoption will accelerate. Regulatory frameworks will clarify as governments recognize stablecoins need appropriate oversight rather than blanket restrictions.

The infrastructure is being built now to support this transition. Early adopters gain competitive advantages through lower costs, faster settlement, and access to new financial services. The technology works. The use cases are proven. The remaining challenge is making integration simple enough that businesses can adopt stablecoins without disrupting existing operations.

We're at the inflection point where stablecoins move from crypto-native applications into mainstream business infrastructure. The next few years will determine which companies, protocols, and jurisdictions lead this transition.

Discover more

.png)

What Are ZK Rollups? Scaling Without Losing Trust.

Understanding ZK Rollups and their role in scaling blockchain networks efficiently.

.png)

Wrapped Tokens Explained: The Trust Problem with WBTC

How wrapped tokens allow Bitcoin to move between blockchains, the counterparty risks this creates, and why atomic swaps provide trustless Bitcoin interoperability.

Bitcoin Fundamentals: Understanding What Makes It Different

An accessible explanation of Bitcoin's fundamentals, covering fixed supply, decentralization, and why recent price corrections don't change its core value propositions.