Unlock Bitcointo DeFi with Native BTC

Cross-Chain Swaps

Cross-Chain Swaps

A layer 2 sidechain for tokenization that opens Bitcoin to DeFi using Atomic Swaps. Truly trustless finance via direct token interoperability without polluting the Bitcoin network.

Inspired by Bitcoin but, engineered for the future. Mintlayer's architecture blends time-tested principles with cutting-edge innovation.

Bitcoin-Inspired

Architecture

Combining Bitcoin's wisdom with blockchain innovation, we've created a powerful tech stack. UTXOs, Atomic Swaps, ZK-rollups, and simplified smart contracts unite for ultimate security and performance.

RWA Tokenization Ecosystem

Get ready for a simple RWA SaaS platform for institutions to deploy tokenized RWA with a simple template. The platform will also assist with built in compliance services.

Native Cross-Chain Swaps

Our Native Cross-Chain Swaps (i.e., Atomic Swaps) enable secure, trustless exchanges across blockchains. Being peer-to-peer, they eliminate intermediaries, wrapped tokens, and counterparty risk, ensuring a secure trustless exchange of assets.

ZK Layer 3

Scaling Solution

We're developing the ZK Thunder Network, a high-speed, EVM-compatible Layer 3 solution on Mintlayer. This upcoming technology combines our Layer 2 security with EVM compatibility and ZK scalability, aiming to significantly enhance Bitcoin's functionality.

Join the Bitcoin DeFi

revolution with ML Coin

Put your ML coins to work. Stake today!

Easily stake your ML coins using our Blockexplorer and Mojito wallet and start earning ML today.

Your window into the Mintlayer Network.

Navigate, view, and verify transactions and blocks on the Mintlayer network with our intuitive and comprehensive block explorer.

Forge the Future: Develop on Mintlayer

Access our open-source code and full node software to develop, contribute, and innovate within the Mintlayer ecosystem, expanding Bitcoin's capabilities.

Your Gateway to Mintlayer, Bitcoin, and Beyond

Start your journey into the Mintlayer Ecosystem.

Securely store your BTC, ML Coins and MLS-01 tokens with Mojito Wallet. Easily access your fund from mobile app or browser extension.

.png)

Mintlayer's tech stack is a unique blend of proven principles mixed with new-age blockchain innovation.

Delivering scalability

Transaction batching shrinks TX size by up to 70%, reducing fees and network congestion. Plus, Lightning Network compatibility is already available, and our very own ZK Thunder, an EVM-compatible L3 execution layer, is coming soon.

Enhancing decentralization

P2P Native Cross-Chain Swaps (Atomic Swaps) eliminate the need for CEXs and liquidity pools. Low hardware requirements promote inclusivity, allowing anyone to run a full node, even on a Raspberry Pi, thus fostering true decentralization.

Security & reliability

Mintlayer prioritizes security with Non-Turing complete smart contracts, limiting complexity and easing audits. Its UTXO model, despite slightly slower block times, enhances overall reliability.

Increasing interoperability

Enhancing blockchain interoperability through Atomic Swaps, enabling secure, trustless exchanges across networks. This technology allows direct peer-to-peer transactions, eliminating intermediaries and easing cross-chain interactions.

Sustainability in mind

The significant reduction in computational demands compared to most other blockchain allows even a low-power device like a Raspberry PI, consuming just 1 to 5 Watts, to efficiently run a Mintlayer node.

Reducing frictions

Mintlayer's native cross-chain swaps, known as Atomic Swaps, significantly reduce frictions in the DeFi space. By enabling the use of native Bitcoin within DeFi applications, they eliminate the need for wrapped tokens or third-party intermediaries.

Incubator programs

Accelerator programs

Grants initiative

Crypto's Best and Brightest:

The Minds Shaping Mintlayer

Our team unites diverse blockchain experts, including veterans from Tether, Binance, and Bitfinex, with crypto pioneers like Charlie Shrem, all dedicated to

revolutionizing Bitcoin's role in DeFi.

.png)

Join our community

Join our community

Join our community

Join our community

Join our community

Join our community

Join our community

Join our community

January 2026 Mintlayer Development Update

January focused on the mainnet hard fork, Mojito wallet stability improvements, and RioSwap preparation for production launch.

.png)

What Are ZK Rollups? Scaling Without Losing Trust.

Understanding ZK Rollups and their role in scaling blockchain networks efficiently.

December 2025 Mintlayer Development Update

December development highlights including Mojito Wallet improvements, Explorer updates, and mainnet preparations for MintFun and RioSwap.

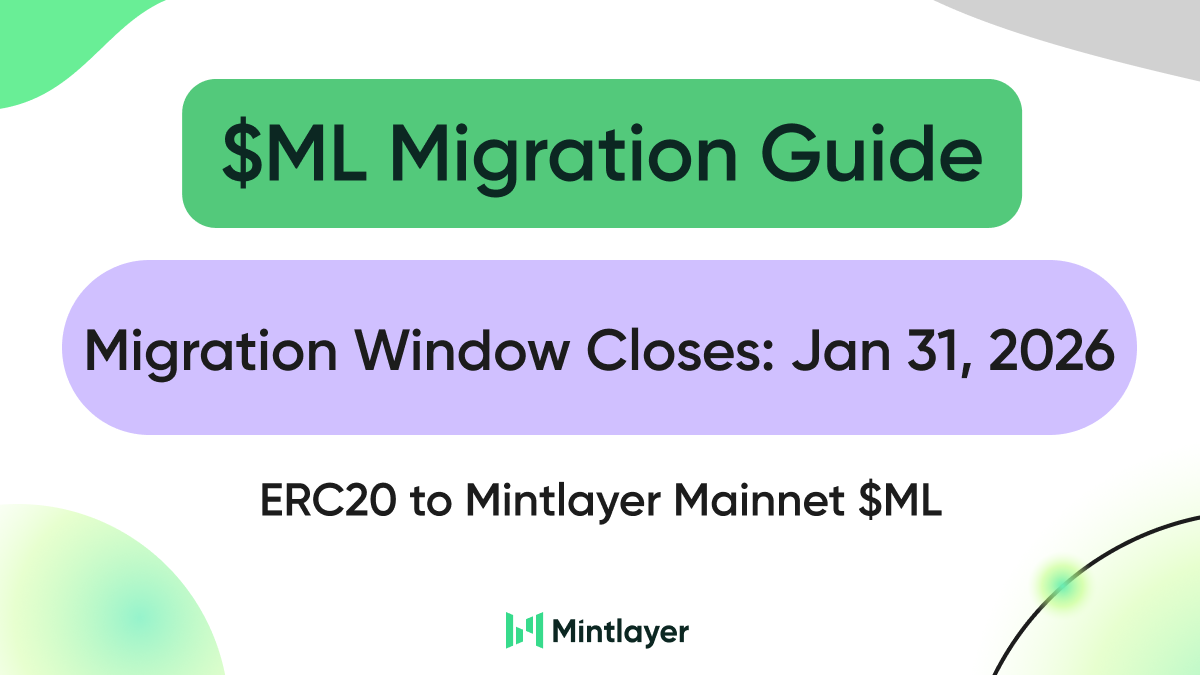

$ML Migration Guide - ERC20 to Mintlayer Mainnet

A guide on how to migrate your ERC20 $ML token to Mintlayer Mainnet coins.

Mintlayer 2025: Year End Development Recap

Mintlayer's 2025 development highlights including RioSwap and MintFun testnet launches, ZK Thunder Network deployment, and Mintlayer Web Services introduction.

.png)

Wrapped Tokens Explained: The Trust Problem with WBTC

How wrapped tokens allow Bitcoin to move between blockchains, the counterparty risks this creates, and why atomic swaps provide trustless Bitcoin interoperability.

Bitcoin’s Hidden Garage: Why BTC Layer-2s Will Be the 2026 Bull Run’s Secret Supercar

An exploration of how Bitcoin Layer-2s unlock DeFi functionality on Bitcoin's secure foundation, positioning them as the 2026 bull run's overlooked opportunity.

.png)

ML Coin Utility: Bitcoin Interoperability & Network Functions

Understanding ML token's utility across Bitcoin interoperability, proof-of-stake consensus, transaction fees, token issuance, and enterprise infrastructure services.

.png)

Stablecoins, Payments, and Asia as the Testbed

Rachel Ong discusses stablecoins as infrastructure, Asia's adoption wave, and bottlenecks to broader business use.

Stablecoins 101: The Infrastructure Layer of Digital Finance

Understand what stablecoins are, why they solve problems traditional banking can't, and how businesses are adopting them for global payments.

.png)

AI Agents, Crypto and the Future of Machine to Machine Payments

How autonomous AI agents could use cryptocurrency for machine to machine payments, and why blockchain infrastructure like Mintlayer is well placed to power that shift.

.png)

November 2025 Development Update

November delivered testnet bugfixes for RioSwap and MintFun, Mojito Wallet improvements, and infrastructure updates as we approach mainnet launches.

Bitcoin and Economic Justice: A Conversation on Closing the Wealth Gap

A conversation with Isaiah Jackson on Bitcoin as a tool for economic empowerment, self-custody, and building parallel financial systems in underserved communities.

Bitcoin Fundamentals: Understanding What Makes It Different

An accessible explanation of Bitcoin's fundamentals, covering fixed supply, decentralization, and why recent price corrections don't change its core value propositions.

Building Better B2B Investments: The Craft of Early Stage Investing

How early stage B2B investing should be craft, not gambling, with insights on transparency and enterprise decision-making.

The Changing of Holders: Understanding Bitcoin's Deepest Shift Since 2017

An analysis of Bitcoin's correction from $125k to the mid-$80s, examining why this pullback differs from past cycles through ownership shifts and global liquidity trends.

.png)

Mintlayer Institutional Suite: Tokenization Ecosystem

Mintlayer's Institutional Suite provides BTC infrastructure for institutions to tokenize RWAs, access regulated yield, and build financial solutions that bridge traditional finance and DeFi.

.png)

What Are Tokenized Real World Assets?

Learn what Real World Assets are, how tokenization works, and why this $30 trillion market opportunity is reshaping blockchain adoption.

.png)

Understanding Mintlayer: From Protocol to Ecosystem

An overview of Mintlayer's evolution from an open source Bitcoin protocol to a complete ecosystem of infrastructure, services, and products.

.png)

Jesse Darnell: How Communities Become Economies

A concise take on Jesse Darnell’s chat with Charlie Shrem, covering communities becoming economies, the U.S. reopening to builders, and how AI plus blockchain is steering capital.

.png)

Why Peer-to-Peer Swaps Matter More Than Ever

A return to Bitcoin's first principles: why peer-to-peer atomic swaps eliminate the trust gap that bridges created.

October 2025 Mintlayer Development Update

Two public Testnets and a core release moved Mintlayer closer to mainnet atomic swaps this October.

.png)

Self Custody 101: Custodial vs Non-Custodial Wallets

Learn the difference between custodial and non-custodial wallets, why "not your keys, not your coins" matters.

.webp)

Is Regulation Blockchain’s Next Real Breakthrough?

A conversation with legal expert Ícaro Avelar on how regulatory clarity is unlocking new opportunities for compliant blockchain innovation.

.png)

From Choke Points to Choice: Rethinking Financial Infrastructure

How the AWS outage exposed the risks of centralization and the need for distributed systems.

MintFun Public Testnet is Live!

MintFun Public Testnet is Live! Find out he full campaign details inside.

RioSwap Public Testnet is Live!

RioSwap Public Testnet is Live! See full campaign details inside.

September 2025 Mintlayer Development Update

September was a month of steady, infrastructure-first progress across the Mintlayer stack.

$16-30 Trillion by 2030: Unlocking the RWA Opportunity

Mintlayer goes deep on Market Metrics and insights on the potential of the RWA market size.

Founders Letter

A message from our founders on our vision, progress, and next steps.

August 2025 Mintlayer Development Update

August was all about shipping a major Core Node release and hardening the path to Native BTC ready infrastructure.

July 2025 Mintlayer Development Update

This month’s updates set the stage for atomic swaps DEX abd dApp integrations.

Bitcoin DeFi Market in 2025: Growth, Potential, and Key Metrics

Bitcoin DeFi is booming in 2025 as yield opportunities and real-world assets attract growing institutional interest.

June 2025 Mintlayer Development Update

Ongoing wallet upgrades, SDK enhancements, and Token Factory testing are paving the way for smoother dApps and Bitcoin-native integrations on Mintlayer.

May 2025 Mintlayer Development Update

With the Token Factory UI, SDK release, and wallet improvements, Mintlayer is paving the way for broader DeFi adoption.

April 2025 Mintlayer Development Update

April’s update highlights progress on the fast bridge, wallet improvements, Explorer enhancements, & the near-completion of the Token Factory.

March 2025 Mintlayer Development Update

Explore Mintlayer’s March 2025 update featuring the ZK Thunder Testnet launch, core protocol upgrades, and Mojito Wallet enhancements.

How to Add ZK Thunder to Metamask

This is a step-by-step guide How to Add ZK Thunder to your Metamask Wallet.

.png)

Mintlayer Unveils ZK Thunder Network L3 on Testnet – Enabling Interoperability & Ultra Fast Settlement

We’re excited to announce the launch of ZK Thunder Network Layer 3 (L3) — ultra-fast, EVM-compatible scaling solution!

February 2025 Mintlayer Development Update

Explore Mintlayer's February 2025 updates featuring core enhancements, ZK Thunder testnet launch preparations, and the opening of early registration for our RWA SaaS platform.

Mintlayer x Joinn - Buy RWAs, Spend Seamlessly w/ DeFi Mastercard

Mintlayer partners with Joinn, a next-gen platform that bridges RWAs with DeFi-powered spending solutions.

Are Quantum Computers a Threat to Crypto?

We break down the risks posed by quantum computing and explore potential solutions to safeguard blockchain security.

January 2025 Mintlayer Development Update

Discover the latest Mintlayer updates for January 2025, including Wallet Connect enhancements, Block Explorer upgrades, and core network improvements.

.png)

Mintlayer x Kylix: Unlocking Native Bitcoin Lending and Cross-Chain DeFi

Partnership announcement with Kylix, a cross-chain liquidity protocol that enables native Bitcoin lending and borrowing

Reflecting on 2024: Mintlayer Development Recap

Mintlayer 2024 Year-End Development Recap - milestones, progress and more.

Mintlayer’s Pulsar Consensus: A New Era for Efficiency & Security

We have published our comprehensive white paper on arXiv.org detailing the Pulsar Consensus.

.png)

Native BTC Cross-Chain Swaps Come to Mintlayer’s Mainnet

Mintlayer Version 1.0.0 Release Date Scheduled for January 15th. That enables Atomic Swaps and improved trading functions.

October 2024 Mintlayer Development Update

Read the post for a huge month of Developments to Mintlayer products.

September 2024 Mintlayer Development Update

Read this post for a full update of September’s development progress.

.png)

August 2024 Mintlayer Development Update

Mintlayer August Development Progress - Atomic Swaps launched on Testnet

.png)

July 2024 Mintlayer Development Update

Mintlayer July Development Progress - find out what the team has accomplished this month

June 2024 Mintlayer Development Update

Mintlayer June Development Progress - find out what the team has accomplished this month

May 2024 Mintlayer Development Update

Mintlayer May Development Progress - find out what the team has accomplished this month

April 2024 Mintlayer Development Update

Mintlayer April Development Progress - find out what the team has accomplished this month

March 2024 Mintlayer Development Update

Mintlayer March Development Progress - find out what the team has accomplished this month

February 2024 Mintlayer Development Update

Mintlayer February Development Progress - find out what the team has accomplished this month

Mintlayer Mainnet Launch Recap

Mintlayer 2023 year in review and Mainnet Launch Recap

Mintlayer Mainnet Launch - January 29th, 2024

Mintlayer is set to launch its mainnet on January 29th, 2024 find out all the details.

Art Meets Blockchain: A Journey Through NFTs and Bitcoin

Uncover the transformation of art and value in the blockchain era through NFTs and Bitcoin upgrades.

November 2023 Mintlayer Development Update

Read this post for a full update of November's development progress.

October 2023 Mintlayer Development Update

Read this post for a full update of October's development progress.

September 2023 Mintlayer Development Update

Read this post for a full update of September's development progress.

Incentivized Testnet: Final Distribution Details

Get the full distribution details on Mintlayer's incentivized testnet program.

A Comprehensive History of Mintlayer's Consensus Evolution

Delve into the intricate journey of Mintlayer's consensus development from its inception to its current state.

August 2023 Mintlayer Development Update

Read this post for a full update of August's development progress.

Mintlayer's Incentivized Testnet: A Guide to Earning More with TML

Learn about the Mintlayer Incentivized Testnet and how you can be rewarded for participating.

July 2023 Mintlayer Development Update

Read this post for a full update of July's development progress.

Mintlayer Public Testnet Launch

We are thrilled to annouce that July 31, 2023, is the date for the highly awaited public launch of the Mintlayer testnet.

Understanding Crypto Staking

Understanding crypto staking's contribution to blockchain operations and the benefits and drawbacks.

Understanding Cross Border Transactions With Bitcoin

Learn about the benefits and challenges of using Bitcoin to send money overseas.

Bitcoin and CBDCs: The Future of World Trade

Learn about the CBDCs and the possible role Bitcoin could play in monetary policy.

June 2023 Mintlayer Development Update

Read this post for a full update of June's development progress.

What Can I Buy With Bitcoin?

Bitcoin is the most prominent digital currency. It may surprise you to learn about all the companies that accept Bitcoin as payment.

What Are UTXOs?

UTXOs are the building blocks of Mintlayer and Bitcoin. Learn about the advantages and challenges introduced with this accounting system

Bitcoin Bridging

Learn how other blockchains introduce vulnerabilities to Bitcoin users and how Mintlayer solves DeFi's biggest attack surface.

Bitcoin Mining Explained

Bitcoin Mining Explained? How does it work, and why is it necessary?

May 2023 Mintlayer Development Update

Read this post for a full update of May's development progress.

Mintlayer ML Staking

Learn about our staking program and how you can engage with the Mintlayer network.

Bitcoin Halving Explained

What is Bitcoin halving? What effect will it have on Mintlayer?

The Problems With BRC-20 Tokens

BRC-20 has caused a stir lately, but is the tech really sound for real life use cases?

The Blockspace Dilemma: Bitcoin Congestion and the Emergence of Inscriptions and BRC20

Exploring Bitcoin's congestion issues and Mintlayer's potential as a solution.

How Mintlayer Adds Value to Bitcoin

Why does the world need another blockchain? Exactly how does Mintlayer add value to Bitcoin?

April 2023 Mintlayer Development Update

Read this post for a full update of April's development progress.

Looking Forward: Mintlayer’s Renewed Focus

As part of our ongoing efforts to revitalize our messaging and energize our community, we are looking forward.

We Are Updating Lightning Network Integration

We are changing the way we support the Lightning Network in the Mojito Wallet.

March 2023 Mintlayer Development Update

Preparing for the TGE and more work on the core. Read this post for a full update of our development progress.

Mintlayer’s ML token will list with Gate.io

Mintlayer is proud to announce the ML token listing on Gate.io

Ticker Change: MLT becomes ML

The Mintlayer token previously known as MLT is now known as ML.

Mintlayer Circulating Supply

Mintlayer's supply has a hard cap, and the circulating supply can be accurately estimated at any given time.

Mintlayer Pre-TGE ML Token Sale

Last opportunity to acquire Mintlayer tokens before TGE.

Mintlayer is Now Partnered With Launchpool Labs

Mintlayer is proud to announce our partnership with Launchpool! Launchpool is a project that connects the varied stakeholders of the crypto community.

What Makes Mintlayer Unique? Key Differences

Mintlayer istn't just another blockchain. It is carefully designed to be capable DeFi platform and interoperable with Bitcoin.

February 2023 Mintlayer Development Update

New browser extension, lots of core development, and work on entropy. Read this post for a full update of our development progress.

The Future of Bitcoin

The future of Bitcoin is so bright, but exactly what it looks like might surprise you.

Nation State Bitcoin Adoption

Bitcoin has the best chance of being adopted as or replacing national currencies in developing countries.

Future Use Cases for NFTs

Mintlayer's unique organizational structure, open source status, and technology stack make it ideal for organizational adoption of NFTs.

January 2023 Mintlayer Development Update

New browser extension, lots of core development, and work on the entropy. Read the post for a full update of our development progress.

.webp)

The Future of Defi on Bitcoin

Mintlayer ushers in the future of DeFi on Bitcoin by removing the need for wrapped tokens and bridges, and building native Bitcoin support directly into the platform.